Book Review: Lifecycle Investing

Asset Allocation is harder that it looks...

Book Review: Lifecycle Investing by Ian Ayres & Barry Nalebuff

Let me start with a confession. When I spouted off in the last letter about how we would figure out the correct asset allocation by the year-end, I had no idea how difficult that topic is and how many layers it has. I spent the first half of October with a growing sinking feeling in my stomach.

So I consider it a solid bit of luck that I ran into an article on that topic in the WSJ (paywall) by Professors Ian Ayres and Barry Nalebuff of Yale University. In an extra bit of luck, it was the type of article that leaves your eyes popping out of the sockets and your beverage spilled all over your pants.

Not for them the wimpy stock allocations of a constant 75% or 100 minus your age. In their book “Lifecycle Investing”, they recommend young people should lever up to a 200% stock allocation and bring it down gradually to 83% by retirement. Told ya!

If you're anything like me, you are probably shouting "Margin Call" at your screens. Or maybe "GFC". Let me put you out of your misery.

They do consider both of those possibilities and more. Reasonable minds can discuss and disagree about how they deal with these scenarios but the authors certainly don't ignore them.

Before you write them off as a bunch of ivory tower academics, Barry co-founded and sold a Tea company to Coca-Cola for more than $100 million. Ian, a law professor, spent $100,000 on long dated S&P500 call options in mid-2009 when, while writing the book, he realized that he was under-allocated to equities. Well done Sir! Well done!

And in an added bit of flex - the book was published in 2010, right after the GFC. It takes a certain amount of… testicular fortitude? to put out something like that right after the biggest market crash of your life time.

Time Diversification

The central insight of the book is that just as diversifying your investments across assets is a free lunch that improves the efficiency of your portfolio, diversifying your investments across time also does the same thing.

You shouldn't just do one, if you can do both.

I am going to assume that most of you know the benefits of diversifying your investments across assets. So what does diversifying across time mean?

Most people (especially salaried employees) invest a lot more in the stock market in the later years of their careers than they do in the early years. This is because your income and savings tends to be quite low early on and gradually increase over time, like the orange line in the chart below.

Lifecycle Investing's thesis is that in this pattern, your investing is heavily concentrated in the later years of your life. Nearly 40% of the total investment happens after the age of 55 and 2/3 after 50! If the market doesn’t do well in this period, you're in trouble. You need time diversification.

To get full benefits of time diversification, your annual investments in the stock market should look more like the teal line. Both lines add up to $1 million over the entire earning life from 25 - 60 but one starts with $3K and ramps up to $100K, while the other is flat at about $30K.

But our intrepid investor does not have $30K to invest when she is 25. She has only $3K. Hence, the leverage. How much?

Lifecycle Investing suggests a cap of 2:1 for a few reasons. Higher leverage would come with higher borrowing costs and higher risks of a margin call. Lower leverage would be sub-optimal.

So the way this works out is that you invest with 2:1 leverage for about the first decade of your investing life and then slowly ramp it down as you approach retirement. This doesn't get you the teal line but it gets you closer.

Back-Testing

The book then devotes two whole chapters to back-testing and Monte-Carlo simulations of this Lifecycle strategy and comparing it against the more traditional asset allocation approaches such as constant allocation and the birthday rules (% of equity in your portfolio = 110 minus your age).

The results are dramatic. The Lifecycle Strategy out-performs both alternatives handily, by 60-90% over a lifetime on average. That’s a lot™.

I am well aware of the pitfalls of back-testing and simulating strategies but I found these chapters more convincing than I expected to. It helps that they also shared with me the real-life performance of the strategy since 2009 and it handily out-performed the alternatives.

In the book, the Professors have made a genuine attempt at tackling the stronger objections to their strategy.

For instance, part of the out-performance of their basic strategy (start with 200% equity exposure and ramp down to 83% or in their notation 200/83) comes from the fact that it simply has higher lifetime equity exposure than the other two strategies.

Those strategies start and end with lower exposures to the stock market. And the stock market has done well in US.

They run the back-tests with a modified strategy (200/50) that eliminates this higher lifetime stock exposure and find that while the mean outcome is the same between strategies, the Lifecycle strategy has lower variance.

This surprised me initially because I was fixated on the 200% equity exposure recommended in early years. How could a strategy with 200% equity exposure have less variance than one with 75%?

The answer is that the 200% exposure is when your savings are very small. So market movements in the early years do not impact the eventual outcome too much, even with leverage.

By the time your savings are larger, the exposure of this modified Lifecycle strategy is lower than other strategies and again the market movements impact the outcome less than for the other two strategies.

What the Lifecycle strategy is doing is that its reducing your reliance on the market performance in later years while delivering the same average return. In other words, time diversification.

This sequencing of returns is a well known problem in retirement planning. If the market crashes just before you retire, your savings take a large hit under the constant allocation model.

The birthday rule tries to fix this by reducing your allocation as you approach retirement. However running a very low equity allocation on the larger savings leads to a much lower lifetime equity exposure, which is also sub-optimal.

The second objection they tackle is that the Lifecycle model works well because the US market has done unusually well over the last century. They run the back-tests for Japan and UK stock markets.

While the data for US is from 1871, the data for UK is only from 1937 and for Japan from 1950. Again the strategy outperforms consistently but the gap really closes in the later years.

This is because the earlier cohorts benefit massively from leverage during the bubble years in Japan. The later cohorts in Lifecycle strategy start to take a lot of pain as the Japanese markets keep crashing for 20+ years but still outperform.

Since their data ends in 2009, we don't know the performance of cohorts that started investing just as the bubble peaked and burst. They ran headfirst with all that leverage into a declining market.

The out-performance of Nikkei since 2012 would further favor a constant allocation strategy for those investors since they would be investing larger amounts in a rising market.

This isn't surprising. Looking at the first chart its obvious that if you get 20-30 years of poor returns followed by a rally, the orange line will do better. The teal line should do better in case the sequence of returns is reversed.

The billion dollar question is which one do you choose when you don't know what you're going to see. On that question a chart above (figure 3.1 from the book) does a lot of heavy lifting.

Notice the Lifecycle strategy gives you a much better worst case outcome, while giving you a slightly worse best case outcome. This is despite having identical equity exposure over lifetime and an identical mean outcome. That seems like a worthwhile trade-off.

There is a lot of other supporting data and arguments in the book. I came away convinced that time diversification does lead to a more efficient portfolio and makes sense. But is it practical?

One Big Objection

Yes! Margin Call! GFC!

Professors Ayres & Nalebuff claim that the Lifecycle portfolio never hit a margin call in the entire 130 year plus historical sample from US or during the 10,000+ simulation runs. Not in 1929, not on 19 Oct 1987 and not in 4Q2008. Not even in Mar 2020. And not in Japan or UK since mid-1900s.

I am not convinced.

They address this exact question at the end of Chapter 3. Their back tests call in the margin loan at the end of every month and rebalance the portfolio to the target leverage level. Managed this way, the model never got a margin call because there was no month in which the market fell more than 33% (even intra-month), the threshold for a margin call on many exchanges.Again,

The worst month apparently was Sep 1931, when the market declined 31.5%.

But it hasn’t happened in the past doesn’t mean it can’t happen. History is littered with dead funds that ran back-tested models with great returns. And 31.5% is awfully close to 33%.

Also, though, who can run their portfolio like this? Most people don't do an annual rebalancing, let alone monthly. The Professors recognize this and in fact recommend quarterly or even annual rebalancing in the book, with a provision for interim rebalancing if the actual allocation varies by more than 20% from the target allocation.

Again, this may work in the model but there is no way most of us can practically implement this. The S&P500 had a peak to trough drawdown of more than 33% starting late Feb 2020 though late Mar 2020. Not many people would have remembered to do an interim rebalance around 28th Feb, when the 20% deviation threshold would have been hit. There were too many other things to worry about. Toilet paper for one.

4Q2008 similarly had a >33% drawdown intra-quarter.

They call for an automated solution like target date funds to deal with both these problems. That may work but that option doesn't exist today. Without one, there is no way the vast majority of us can be certain of avoiding a margin call with 2:1 leverage.

Time Diversification vs. Asset Diversification

It doesn’t make sense to borrow at an individual level to invest in fixed income. There's no spread.

So running a 200% equity exposure in early years means you have no fixed income exposure for a fairly long time. In other words, you are giving up asset diversification for the sake of time diversification. Is this efficient?

Figure 3.1 above showing a narrower range of outcomes for the Lifecycle strategy shows it may be. But asset diversification as a free lunch is such an established principle of investing that I would want a lot more than a back test to overturn it.

The Professors also point out that most people can think of the present value of their lifetime income as a bond, although its not a very diversified exposure. Seen this way, in the early years of your career, you are already very over-allocated to fixed income. Leveraging stock exposure only reduces that a bit.

Efficient Leverage?

Leverage is just so much better in real estate - its cheaper, you get more of it and there's no mark-to-market. What's not to like?

If you take a holistic view of your risk asset exposure (rather than just equity exposure) maybe the conventional path is already quite efficient in providing time diversification.

A 30 year old with $100K to invest will get much better time diversification buying a house with 5x leverage than buying stocks with 2x, with a pretty low risk of a margin call. That's what most people do already. So why bother with the complexity of a leveraged equity portfolio?

This is what Prof. Nalebuff had to say in response to my question on this topic:

"Just as you want to have a broadly diversified equity portfolio (including commodities), you should want to have real estate in the portfolio. In theory, to get an perfectly even exposure to stocks over time (and thus ideal time diversification), one would want to have 10:1 or even 20:1 leverage with equities when young. But margin calls and the cost of borrowing make that infeasible. You can, however, do this safely with real estate. So I would propose using leverage for both equities and real estate."

I suppose that boils down to your risk appetite. Just how much leverage are you comfortable with? Having started investing in Banks during the GFC, I have bad feelings about leverage but that may not be true of everyone.

Taking it down a notch

Chapter 6 of the book tackles the cases where this strategy does not apply.

A simple case is if you have high cost credit card debt, you should pay it off first rather than borrow more to invest.

Another case is people whose income is heavily linked to the equity market e.g. investment bankers. They can think of the net present value of their income as part of their total equity exposure (instead of as a bond) and shouldn't top it up with leverage in the portfolio.

The Professors also point out that leverage should only be applied to long term investments e.g. for your retirement portfolio. If you're saving for other goals, say down payment for a mortgage or college fees for your kids, you shouldn't lever up those portfolios.

In effect this means that they are not recommending 2:1 leverage on your entire portfolio but only on a portion of it, which reduces the overall leverage quite a bit.

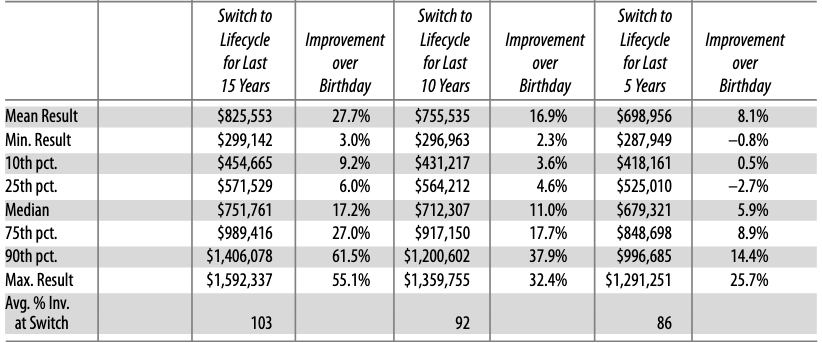

Think of the children

What if you are already in your 40s and 50s? Is it too late for you to benefit from this strategy? The Professors show that switching to the Lifecycle strategy has some benefits even if you do so in the last 10 years of your earning career.

They also suggest that if you can afford it, you should gift your kids a leveraged portfolio early in their life. This will have a large impact on their lifetime exposure to stocks. Time diversification works better when you have more time.

Bottom Line

Lifecycle Investing has forced me to rethink some key assumptions about managing my personal portfolio. There is a lot more in the book that I have left out and it deserves multiple readings.

The context in which I read the book was laid out in the last letter here. In short, many of us may live to 90 or more and we may be much more active than our parents at advanced ages. That more active lifestyle will need more money to support it. Commonly used asset allocation methods like the Birthday Rule or Constant Allocation (75:25 or 60:40) may not get the job done.

I was already considering more aggressive asset allocation strategies when I wrote that but the word "leverage" wasn't in my retirement dictionary. I now wonder if it should be.

I also opened sub-accounts for both my kids at Interactive Brokers (totally painless BTW) and am considering using some leverage for that portion.

But 2:1 may still be a bridge too far for me or for them. In the form it was back-tested, and with the investment options available today, it simply cannot work for most individuals. The behavioral issues and tail risks are too large.

Does 1.25:1 still risk a margin call? What about 1.5:1? TBC.

The nudge

Get set for investing in Singapore Savings Bonds (SSB) and Singapore Govt. T-Bills.

The yields on both these instruments have shot up in the last few months. In the latest auction, on 27 Oct 22, the 6 month T-Bills were allotted at a yield of 4.19% while the SSBs had a yield of 3.08%. That's better than most deposit rates and even what the Robo-Advisors offer on their cash management products.

While there is a capacity constraint on SSB (maximum allocation was S$10.5K in Oct 22), non-competitive bids for T-Bills got 100% allocation. So these are good options if you have some spare cash that won't be needed immediately.

SSBs can be liquidated in 7-35 days (read more here) and T-Bills can be sold in the market anytime or redeemed at maturity (6m & 1y).

What do you need to invest in these instruments? 3 things:

An account with a local bank i.e. DBS, OCBC or UOB

An account with the CDP

Set up a Direct Crediting Service (DCS) between the CDB and your bank

Most people should already have an account with a local bank. If you don't then this is possibly the hardest step.

Opening an account with the CDP takes a couple of minutes with your SingPass. In fact, if I recall correctly, you don't need to "set up" anything. If you have SingPass, you just log in.

The process for setting up the DCS varies by your bank. With DBS, I just needed to send one SMS and the DCS was ready in a few days. Its quite painless.

If you do this now, the account will be ready in time for the next auction.

This month in moolahgeeks

October was a light month on moolahgeeks as I spent a lot of time working on launching the India site. The beta version should be live by the time you read this.

One of my goals at moolahgeeks is to provide "actionable" content. I felt the last piece from September on cash management fell short of that ideal and was my first inkling that asset allocation would be a hard topic to cover. If you have a question or suggestion about how to manage your cash better, please let me know and I will try to incorporate that.

Credit Card Sign-up Gift Game I knew that many people sign up for credit cards only to collect the welcome gifts. What I didn't know was just how popular this game was. An investment banker, a fund manager, a CMO and a start-up founder with a successful exit, all told me with some degree of pride, that they were enthusiastic players.

So I dug into the rules of the games and the potential pitfalls that await newbies. I found you can earn about S$1,000 a year playing this game, at about S$200 / hr. It won't fund that retirement in the Mediterranean but it will pay for the ticket.

Travel Insurance Staying with the travel theme, I looked into the best Travel Insurance in Singapore as I prepared for the much awaited COVID-19 revenge travel in December. I did not know there were at least 18 travel insurers in Singapore and I did not expect such a wide range in pricing or product features.

A basic annual family plan for worldwide travel can cost anywhere from S$460 (HL Assurance) to S$2,500 (Allianz). And here's the kicker - the HL Assurance plan has better coverage and better customer reviews than Allianz.

This one's actionable for sure - save yourself some money. Safe Travels!

Finally, I want to welcome Kshitiz V Sharma to the team. He joined me in August after completing his post-graduate diploma from Indian Institute of Mass Communication. He has been a huge help in getting the India site up and will continue to lead that effort.

Around the web

Mr. Beast seeks $1.5Bn valuation Mr. Beast is something of an obsession for me. Not his YouTube Channel. I have seen only one of his videos. But his life story is simply incredible and inspiring. Started his YouTube channel at 13, persisted in obscurity for years, optimizing continuously. Viral but not an overnight success. Here's a thread on his business model.

First YouTube billionaire but will he be the last?

Can you make money in meme stocks? "Consistent with models of attention-induced trading, intense buying by Robinhood users forecast negative returns. Average 20-day abnormal returns are -4.7% for the top stocks purchased each day."

Switzerland’s environment minister suggests people shower together to save energy The best personal finance advice this year. You heard it here first.